P.R. Popcorn Alert: “I Hate Math!” Anti-Mantra Cracks Under PRSA’s $5 Mill Error

The Public Relations Society of America’s (PRSA’s) latest balance sheet unveiled on December 20, 2023, is more than $5 million out-of-balance, without acknowledgement or explanation from PRSA leadership.

That’s the headline. But there’s more to this story.

Much more… as in, it’s time to fire up your microwave with your favorite popcorn bag of Orville Redenbacher and dig in for a 25-minute read.

For those unfamiliar with the public relations industry’s primary trade organization in the U.S. that enjoys 501(c)(6) tax-exempt status, PRSA describes itself as “the leading professional organization serving the communications community… Guided by its Code of Ethics…”

As such, PRSA is supposed to operate honestly, ethically, and transparently.

Its national board and staff leadership are obligated to model the ideal behaviors of integrity and truth-telling that all members of the PR industry should embrace.

By law, PRSA’s leaders must exhibit honesty, disclosure, and transparency when it comes to matters of PRSA’s own financial stability and solvency when representing itself to dues-paying members and government agencies.

But that’s not what PRSA leadership has delivered, for many years now.

Along those lines, here’s an anecdote from some years ago, back when I was a PRSA member myself, attending the PRSA International Conference.

In October 2016, I observed — as a former PRSA National Board member myself (2002-03) — the PRSA Leadership Assembly in Indianapolis, Indiana.

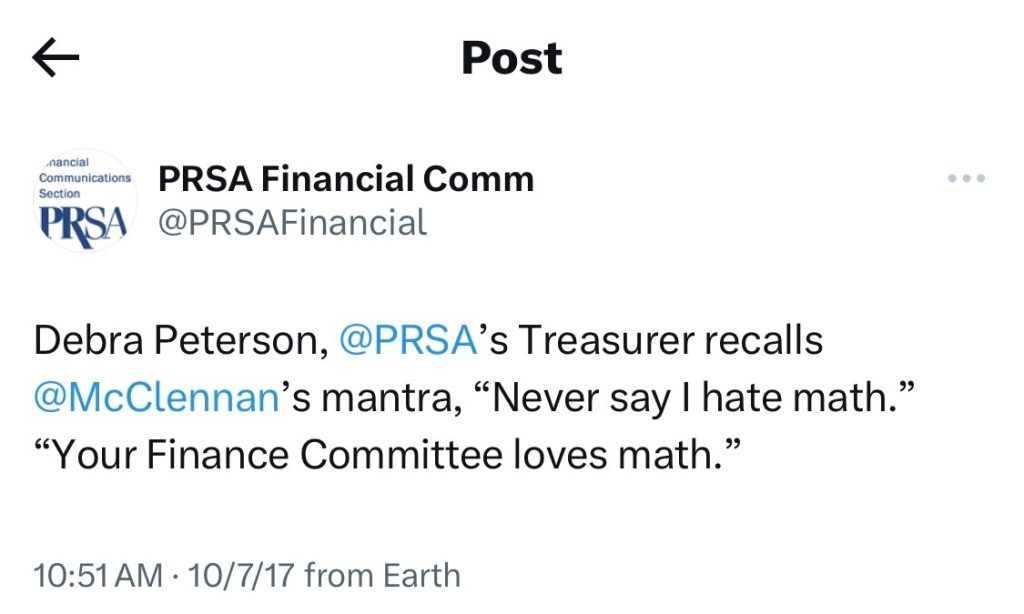

Standing at the Assembly microphone, then-PRSA National Chair Mark McClennan issued a friendly scolding to the delegation of hundreds of PRSA leaders, admonishing anyone in our language-arts-and-sciences-centric field for ever having uttered the words, “I hate math.”

Polite applause registered from many delegates, in solidarity with the Chair.

After all, his clarion call seemed clear and justified:

We PR pros should make a clean break from our stereotypical math-phobia shackles of the past!

Never again should we fail to whip out our Texas Instruments at any opportunity to add, subtract, or figure out where the decimal point goes!

We as PRSA members should and must embrace PRSA’s fabulous financials and metrics and all-things-quantitative-data!

…Or, at least that was the basic drift of McClennan’s commentary. And, truthfully, at the time, who could argue?

McClennan tweeted his own self-praise as “a stand-up leader,” for boldly holding all of us PRSA rank-and-file folk accountable…

The grandstanding episode suggested that getting into the financial nitty-gritty was a newly declared PRSA love-language, on a going-forward basis.

But several years later, the other shoe dropped.

In December 2020, Past Chair Mark McClennan signed his name to an expulsion order, which I personally received, literally in writing.

McClennan and numerous past chairs of PRSA — desperate to protect their own national chairmanship legacies in the organization by deflecting any criticisms toward the PRSA brand or themselves — sought expulsion of and deep reputational harm toward me, and me alone.

Their crusade sought to have me ousted from PRSA membership, on the heels of my having asked some math questions of my own that were not to their liking.

When they couldn’t (or wouldn’t) produce any logical or defensible answers to my questions, I then asked these math questions publicly, about obvious PRSA National financial reporting discrepancies of 2018, 2019, and 2020.

I identified the discrepancies to be in the millions of dollars.

How?

Simple math.

I compared PRSA’s Board-approved, written Assembly minutes — which documented many claims of financial stability made by PRSA National Chairs and National Treasurers each year at the annual Assembly meetings — alongside PRSA’s audited financials.

The financials were customarily posted on the MyPRSA member-only intranet at a much later date… in fact, usually more than half-a-year later, after delegates had long-since forgotten about the prior Assembly and whatever claims and assurances had been made by leadership at that event to the voting delegation.

I then further compared those sets of claims / numbers with PRSA’s annual United States Internal Revenue Service (IRS) Form 990 tax filings… which PRSA is required to file as a legal document, to maintain its IRS tax-exempt status.

PRSA’s 990s were only made available even much later (usually, more than one year after the PRSA Assembly for which the financial reporting year in the Form 990 correlated).

In reviewing these materials for each year, side-by-side, PRSA Inc.’s financial discrepancies were clear as day.

There were a lot of them. And they were not small.

Over the years in question (2018-Present), McClennan’s camp of PRSA National Chairs had been reporting one set of “All is well!” financial messages to the Assembly’s voting delegation – devoid of state-law mandated financial records and specific dollar figures – while later, PRSA’s staff CFO quietly filed IRS Form 990 tax returns reporting different financial data entirely.

(More on IRS revelations documenting false PRSA-provided data in the government’s possession, in a minute).

News of the financial discrepancies that I had uncovered didn’t exactly sit well with the PRSA leaders responsible for the discrepancies.

McClennan’s (and his like-minded colleagues’) response: Kill the messenger.

Taking such a tactic is, of course, in multiple violation of the PRSA Code of Ethics, which — among other things — actually states in writing that a PRSA member must “Report practices that fail to comply with the Code, whether committed by PRSA members or not, to the appropriate authority” (see “Enhancing the Profession” provision).

I indeed had reported failures to comply with PRSA’s code to the “appropriate authority.”

The problem, however, was that the “appropriate authority” in this case was composed entirely of the very people “fail(ing) to comply with the Code”: PRSA National leadership and their paid executive staff.

Violating PRSA’s own ethics code didn’t seem to stop these individuals in the past from any range of misdeeds — so they certainly weren’t going to be stopped from doing so again, in the name of safeguarding their own self-interests.

So they retaliated against me, in a highly premeditated, orchestrated, and illegal expulsion of my more than 25-year PRSA membership.

2018 PRSA Chair Anthony D’Angelo of Syracuse University’s Newhouse School joined McClennan and his past-Chairs of like mind, in a tightly orchestrated chorus demonizing me.

They charged that I was “uncivil” and “unethical” for “harming” PRSA’s “reputation,” by my daring ask such math-related questions as “Where is the money you told us was supposed to be here?” and otherwise for my having held these leaders accountable for ignoring my questions or giving completely false replies inconsistent with clear documentation.

There was a PRSA cover-up going on, in full disinformation mode to purposely mislead and deceive PRSA’s members and the larger industry.

In fact, PRSA decided to get especially crafty, on that particular point, in 2021.

To distract from their own disinformation tactics, PRSA National launched a purported anti-disinformation campaign (innocently branded as “Voices 4 Everyone”) — co-chaired by individuals highly implicated in prior year’s financial falsehoods and / or cover-ups of PRSA’s ethics failures — claiming to condemn the very tactics that they were quietly engaged in themselves.

In effect, “Voices 4 Everyone” has been a gaslighting campaign, which typifies most PRSA National communication about anything tied to its own operational, financial and governance failures.

- PRSA has engaged in this kind of diversionary gaslighting on the topic of ethics (pontificating about ethics publicly while violating ethics tenets privately and profusely).

- They’ve engaged gaslighting on the topic of diversity (pontificating about how important diversity is publicly while failing to deliver PRSA’s own diversity promises in a credible or meaningful manner).

- They’ve engaged it on the topic of civility (pontificating about how important “civil discourse” is, all the while demeaning, undermining, and censoring any ideology that doesn’t fit in lock-step with their own preferred political agenda).

- They’ve engaged it on the topic of valuing PR students (pontificating about the importance of PR’s future generation, while so egregiously under-serving PRSSA student chapters that the student organization has now dwindled to 5,772 members, from a high about 10 years ago of 11,500).

All recent National Chairs of the PRSA organization signed their names to the expulsion order targeting me, knowing full-well the many unanswered private reports I had issued directly to them and via the member-only MyPRSA intranet discussion board, asking for explanations about financial losses and discrepancies:

- Garland Stansell (2020)

- Michelle Olson (2021)

- Felicia Blow (2022)

- Michelle Egan (2023), and

- 2024 Chair Joseph Abreu, who himself chaired the three-person “Grievance Panel” in 2021 that “investigated” me and voted unanimously that I was “guilty.”

(Central to Abreu’s manipulation of PRSA’s 2021 kangaroo court, he allowed for one of his two fellow voting Grievance Panel members, Karen Swim, also to be named in the McClennan, D’Angelo, et al., complaint against me that the Panel was adjudicating, as an allegedly “aggrieved” party herself. This planting of a co-complainant essentially inside the jury box violated PRSA’s “conflict of interest” provision in its own Code of Ethics by allowing Karen Swim to vote as a “juror” in a matter wherein she held alleged “complainant” and/or “witness” status. This maneuver violated New York law for willfully and purposely allowing a conflict of interest to which the PRSA National Board and its legal counsel were privy.)

Having cut me off the membership roster without fear of accountability, culprits of PRSA’s misconduct were now drunk with power and emboldened.

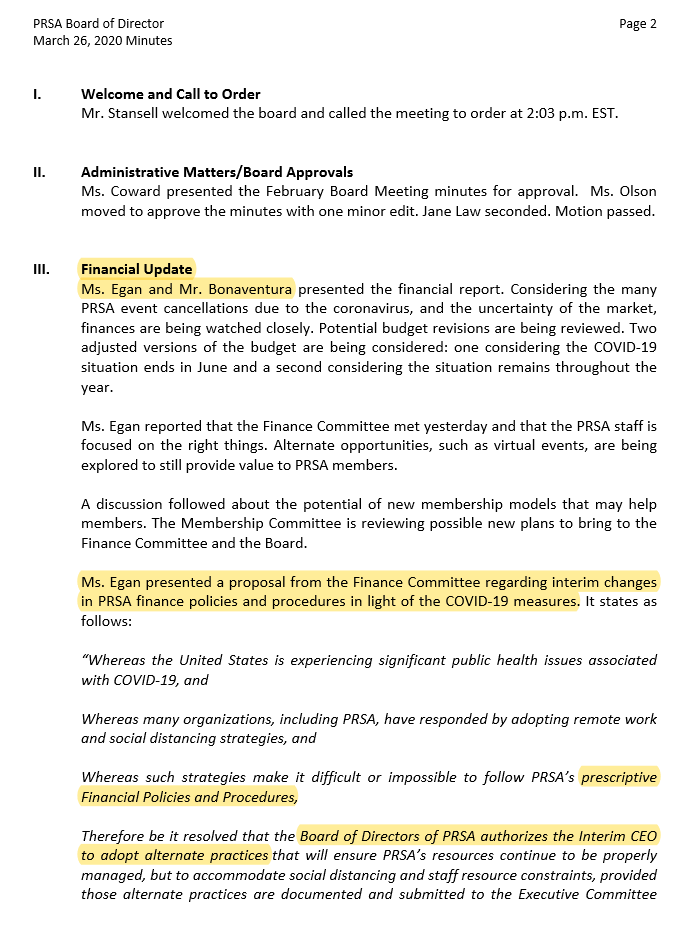

When the pandemic had hit in 2020, PRSA’s then-Treasurer Michelle Egan had led a Board vote to loosen internal financial controls, not enhance them.

PRSA staff CFO Phil Bonaventura — who then was reporting to himself as dual CFO + “acting CEO” during PRSA’s protracted 18-month CEO search — urged the Board to go along with the motion to loosen PRSA’s financial checks-and-balances.

The National Board foolishly voted in favor:

After having me ousted from membership in early 2021 on false and cooked-up accusations in a conflict-riddled process, PRSA’s financials of 2021, 2022, and 2023 reflected even more operational losses and/or discrepancies, into the seven-figures of evaporated member dollars, compounding the earlier seven-figure discrepancies I already had identified for 2018, 2019, and 2020.

And then, just this past month (December 2023): another shoe dropped.

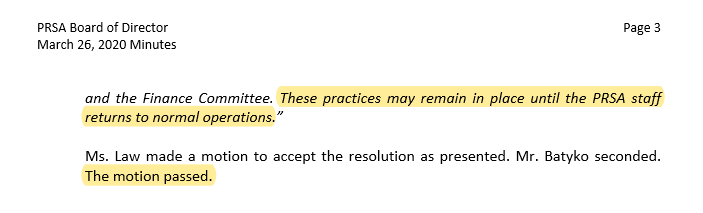

Weeks ago, just before Christmas 2023, PRSA posted on its public-facing website a legally non-compliant 11-month 2023 “Year in Review” balance sheet, inclusive of 2022 balance sheet numbers for comparison.

In PRSA’s customary violation of New York law since 2020, the “Year in Review” brochure’s balance sheet annual report to members did not cover a 12-month time period, but only 11 months — yet again depriving dues-paying members of a full-picture view of PRSA’s year-over-year financial health.

This partial balance sheet has one column for the current year, and a comparison column for the same time period in the year prior.

But in the 2023 “Year in Review,” PRSA leadership did something additionally strange:

They retroactively changed financial data in the prior year’s 2022 published balance sheet.

Not only did 2023 PRSA Chair Michelle Egan, CEO Linda Thomas Brooks, and CFO Philip Bonaventura retroactively change the prior year’s 11-month “Year in Review” balance sheet column for 2022, but also they “forgot” to recalibrate their math accordingly to tabulate simple addition in two “liability” sub-columns that they themselves were responsible for reporting correct data.

Here was the original balance sheet reported by 2022 PRSA Chair Felicia Blow and CEO Linda Thomas Brooks in PRSA’s 2022 “Year in Review,” in December 2022:

Here is the original balance sheet reported by 2023 PRSA Chair Michelle Egan and CEO Linda Thomas Brooks in PRSA’s 2023 “Year in Review” in December 2023:

Below are my own markings on the above 2023 version of the “Year in Review” balance sheet, to underscore the problems with PRSA’s retroactively changed 2022 numbers:

As is clear above, the 2022 column was retroactively altered in 2023, in two places, but without explanation anywhere in the “Year in Review” report.

The two new line items dumped into the 2022 Liabilities section included “Amounts Due to Related Organizations, Net” and “ROU Liability (Leases).”

Bizarrely, the “Amounts due” amount cited under Liabilities of $4,866,925 is precisely the same amount cited much further above in the Assets section for “Investments.”

It makes no sense that these numbers are identical.

Further, both sections in the 2022 Liabilities area where the two new line items were dropped still carry the same subtotals as were in the original 2022 Balance Sheet… meaning, it appears someone (CFO Bonaventura?) forgot to recalculate the math through simple addition.

The resulting balance sheet discrepancy totals $5,411,085.

Consequently, due to PRSA’s math errors by Mark McClennan’s compadres, the 2023 financial statement is more than $5.4 million dollars out-of-balance.

And nobody caught it, before publishing it and posting it for the public record.

Take that in, for a minute.

5.

Point.

4.

Million.

Dollars.

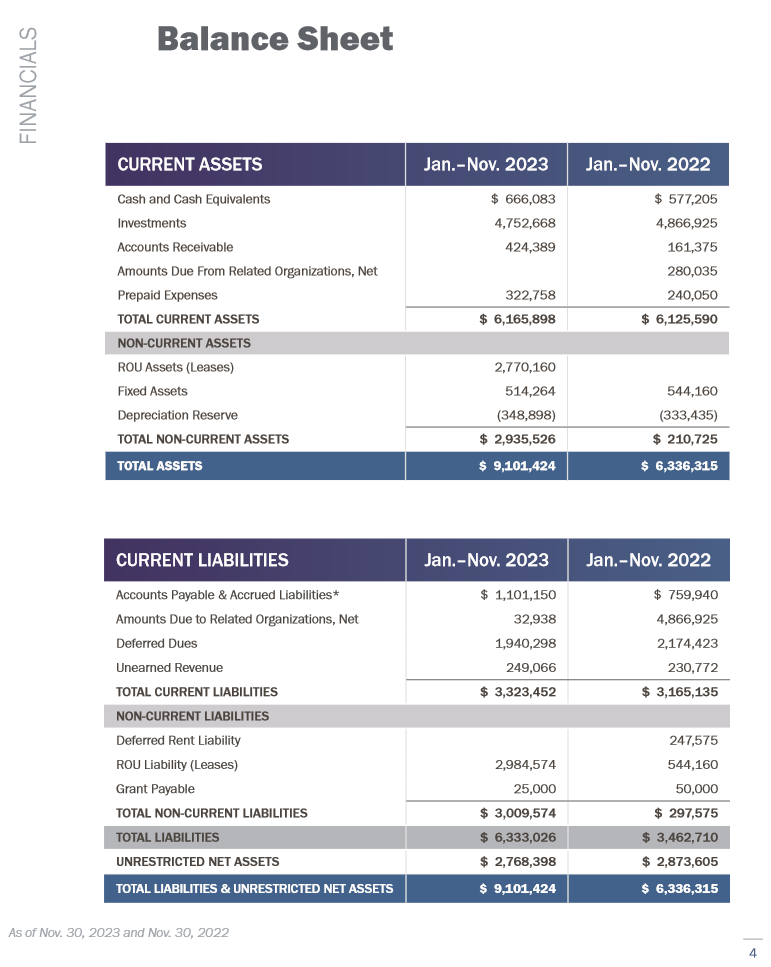

For comparison, PRSA, Inc.’s IRS-reported 2022 gross receipts were $13,547,834:

PRSA, Inc. is therefore sporting a financial discrepancy in its PUBLISHED BALANCE SHEET in an amount nearly 40% of its entire gross receipts for 2022.

To boil it down to a lowest-common-denominator for the folks who scream that “I hate math!” is bad… but who nonetheless can’t be bothered to DO math… this situation is rather a big deal.

At this writing, however, the folks in charge of correcting the record are still checked-out on winter vacation.

While many PRSA members have blindly trusted PRSA National’s dismissive assurances that PRSA’s Finance and Audit Committees receive annually a “clean audit” stamp of approval from its third-party audit firm, the membership might want to take some time – as I have – to dig up the dirt on those “clean audit” claims.

As a first order of business, they might wish to take a quick gander at the January 2022 Public Company Accounting Oversight Board (PCAOB) “Order Instituting Disciplinary Proceedings, Making Findings, and Imposing Sanctions” against 15+ year PRSA tax preparer + “auditor”:

…PKF O’Connor Davies, LLP.

Here’s Page 1 of that 17-page document (and by the way, you might want to grab some more popcorn before reading it):

This scathing report follows a separate, well-known U.S. Securities & Exchange Commission fine against PKF O’Connor Davies in 2016, involving PKF’s issuing a false audit finding for a government municipality… you know — the kind of audit upon which the terms of public bond debt are issued.

Despite these concerning reports about PRSA’s own third-party auditor (which also is the firm that prepares PRSA’s and PRSA Foundation’s IRS Form 990), PRSA CFO Phil Bonaventura apparently saw no reason to recommend to the PRSA Board a new RFP for audit services for the specific purposes of changing auditors due to these horrendous appearances of current-auditor quality-control problems.

Still feeling super-confident in that “clean” PRSA and PRSA Foundation audit?

Still feeling super-confident that everything in PRSA’s IRS 990s are on the up-and-up?

If you do, you’re not very discerning — at all.

But as such, you’re a shoo-in for the PRSA National Board!

Michelle Egan, for example, was a shoo-in.

When she ran for PRSA National Chair, no one even bothered running against her. Everyone seemed to know that the fix was in. She had served two contiguous years herself as PRSA National Treasurer, overseeing PRSA’s massive discrepancies and dollar losses in 2020 and 2021 under claims of clean-audit purity.

During all of 2023 as PRSA National Chair, Egan sashayed all over the continental U.S. and her home state of Alaska this past year, claiming “ethics” as PRSA’s “North Star”:

For context, this gaslighting behavior is typical of Egan. It’s also vintage PRSA.

Relative to Egan (or anyone), I don’t make accusations lightly or without copious evidence.

Over years of the past decade, for example, Egan’s employer (an Alaskan oil pipeline company with a deep, prior history back in the 1990s of major pollution violations and whistleblower retaliation) paid untold tens of thousands to Ethisphere in its for-profit “World’s Most Ethical” program, in order to collect – literally – a “World’s Most Ethical” trophy and bragging privileges.

Egan postured and leveraged heavily this company-paid accolade in her own PRSA political ramp-up… first, to get on the PRSA National Board in the first place, then later to score the PRSA National chairmanship for herself.

According to a June 2020 Bloomberg report, Alyeska was cited in 2020 with a new batch of safety fines — with Egan having been quoted as the company spokesperson in the story.

Shortly after, Egan told PRSA members during a national PRSA Board of Ethics & Professional Standards webinar on September 8, 2020 (which included future PRSA Grievance Panel member + alleged simultaneous complainant Karen Swim), that Alyeska wouldn’t be pursuing Ethisphere’s “World’s Most Ethical” trophy again in the near term, “simply because of the amount of work it is,” she claimed.

Egan’s diversionary rationale completely failed to acknowledge her company was then newly fined by authorities yet again for more operational safety violations.

Earlier, Egan even appeared on Mark (“I love math!”) McClennan’s so-called “Ethical Voices” podcast in December 2019, as part of this posturing / leveraging campaign to advance her PRSA Board career.

But by the end of this past year – in December 2023 – actually doing the due-diligence work of a PRSA National Chair became unimportant to Egan — evidenced by her chairmanship year concluding with a $5.4 million published balance sheet discrepancy.

Apparently, Egan was too busy polishing her newly minted “PRSA Past President” medal to bother with her own fiduciary duties.

Egan was photographed a few months ago, alongside what 2022 PRSA Chair Felicia Blow described as an “amazingly amazing group of leaders,” with like-minded predecessors McClennan, D’Angelo, Stansell, Olson, and, of course, Blow.

Thirteen of the 15 people in this photo below signed their names to have me expelled from PRSA membership for making PRSA look unfavorably with my reports of PRSA National ethics violations, financial discrepancies and other misconduct. The only two who didn’t participate as signatories were the two ladies seated furthest left in the front row, in red and in white, respectively.

The cynicism and hypocrisy of this situation – and the all-out carelessness, negligence, and self-servitude of these people – make me sad for the U.S. PR industry… that this apparently is the best our U.S. industry can do in the “business league” department.

Not sad, but unnerving and even alarming:

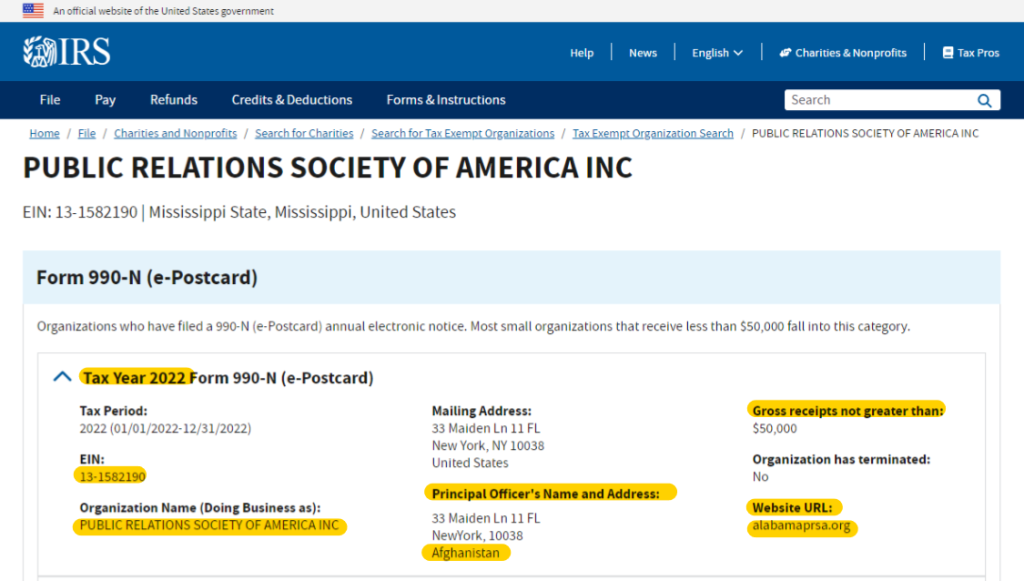

I’ve uncovered serious – even fishy – IRS documentation tied to PRSA, Inc.’s Employer Identification Number (EIN), which, for the record, is 13-1582190.

There are scores of PRSA chapters across the U.S. that each have their own separate EIN number because they file as separate entities with the IRS, which is proper. With that said, this 13-1582190 number is unique to PRSA, Inc. as the corporate entity of the PRSA National organization. Likewise, the PRSA Foundation also has its own EIN number as well.

Just about a month ago, I started looking around the public-facing IRS searchable database for PRSA, Inc.’s tax records, given that PRSA has not appropriately filed via the New York State Charities Bureau PRSA’s 2023 auditor letter validating its prior 2022 financials.

But what I found on the IRS website wasn’t much in the way of current PRSA records.

Instead, what I found were historical PRSA documents of jaw-dropping significance.

As a starting point, it appears that PRSA’s “Principal Officer” is based in Afghanistan… at least, according to the IRS database for the PRSA, Inc. 13-1582190 EIN:

So… that’s breaking news.

In addition, PRSA hasn’t been located on “Maiden Lane” in Manhattan in many years.

I posted a public query directly to CEO Linda Thomas Brooks earlier this past December, asking why Afghanistan (and other weird stuff) was listed on the IRS website for PRSA.

She ignored me.

This EIN number is also erroneously cited via the IRS database as being domiciled at “Mississippi State,” with gross receipts “not greater than: $50,000,” and with its primary website being alabamaprsa.org — all patently false.

For whatever PRSA’s snafu in having Afghanistan listed as such with the IRS, it’s not a good look for PRSA, Inc. – which applied for, and received, some seven figures of “forgivable” taxpayer-funded pandemic PPP lending from the federal government.

It also constitutes fraud for any organization to have applied for such government funding under false / misleading financial statements.

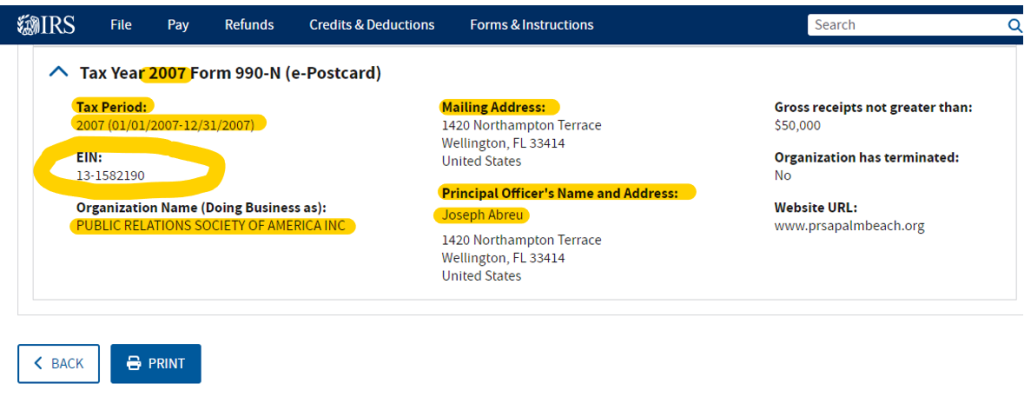

When I scrolled through the IRS’s online record of PRSA’s receipt of annual IRS 990-N postcards (which are supposed to be sent only to “small exempt organizations” with “annual gross receipts…(of) $50,000 or less”), I found a strange litany of records tied directly to PRSA, Inc.’s 13-1582190 EIN number.

A postcard correlating to PRSA, Inc.’s EIN was sent to the residential home mailing address of one “Joseph Abreu,” back in 2007, when Abreu was only a local PRSA officer in a Florida chapter:

As a public record, this same home mailing address is dually noted in a Florida chapter event brochure dating back to 2007 that also still exists in the online domain, documenting that it correlates to Abreu’s then-home address:

Three years after chairing the “Grievance Panel” to have me ousted from membership for asking too many math questions and other perceived “reputational” offenses – Abreu has now taken the helm as PRSA’s 2024 National Chairman.

Now, a question:

Why on earth would any documentation tied to PRSA, Inc.’s IRS EIN ever have been mailed to Abreu’s home mailing address back in 2007, more than a full decade before Abreu ever even joined PRSA’s National Board?

In consideration of this curiosity, one must ask not simply WHO is Abreu, but WHAT is he?

Is Abreu a PR guy?

Or, is he an attorney… whether “practicing” or not?

When Abreu is showboating in the PR industry (or, alternately, quietly crucifying anyone asking valid PRSA math questions), he cites his name as “Joseph Abreu, APR” (with APR designating “Accredited in Public Relations”).

But when he’s seeking a personal magazine profile of himself in a law publication to spotlight his cupcake-baking skills and affinity for cruise ships, in his local market of Lee County, Florida, he suddenly morphs into “Joseph Abreu, Esquire.”

Below is his “Esquire” claim as an apparent member of the Lee County Bar Association:

While Abreu blushingly offers this disclaimer within his puff piece – “…I don’t practice law…” – his use of “Esq.” after his name clearly connotes appearances of a professional claim of having attended and graduated from an accredited law school and/or passed the Florida Bar exam.

Any uncredentialled non-lawyer’s remark of “I don’t practice law” is about as absurd as making a similar comment of, “I don’t practice medicine” by anyone never having been admitted to medical school.

Both comments automatically IMPLY that one holds the requisite education, skills, certifications, and licenses of “practicing” in either field, but that one simply opts not to do so by personal choice, even though they technically could.

The whole thing smacks of an all-out lie.

By using “Esquire” after his name without credentials, there are appearances of intent to deceive.

Such an intent breaks multiple values and provisions of the PRSA Code of Ethics, notably the Code’s requirements under “Advocacy,” “Honesty,” “Expertise,” “Independence,” “Loyalty,” “Disclosure of Information,” and “Enhancing the (PR) Profession.”

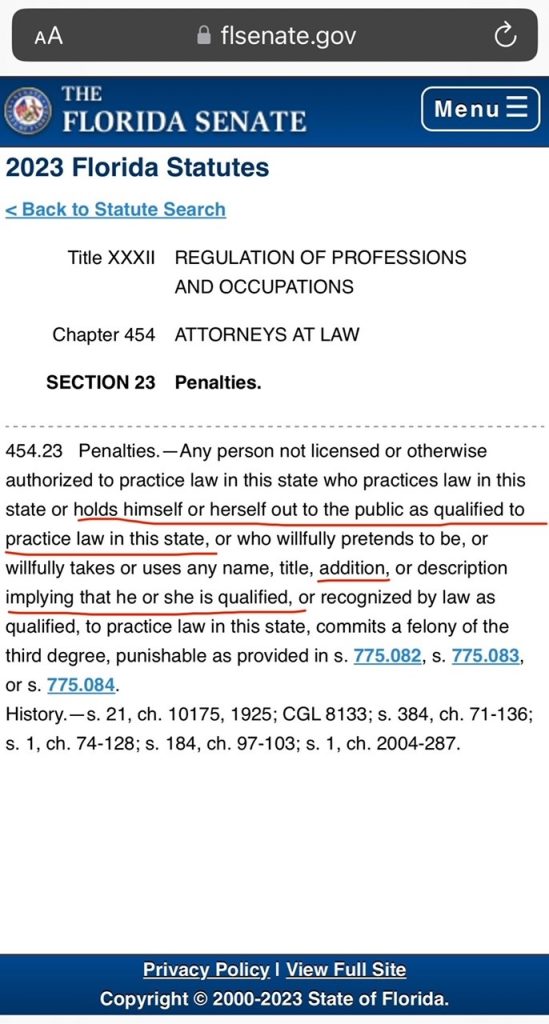

For Abreu, operating in the completely unregulated field of PR, perhaps it never dawned on him that there might be actual legal consequences in the State of Florida for even implying one is an attorney / officer of the court… when one most laughably is not.

Bear witness to this snippet of the Florida State Code, which doesn’t kid around about this stuff.

In Florida, falsely implying you’re an attorney is a third-degree felony:

Back in PRSA National Leadership Land, encountering this level of stupidity is, sadly, what our PR industry in the United States is reduced to having itself represented by, to the entire world.

We’re saddled with incompetent, oblivious volunteers being elevated to national governance board positions in a primary trade organization, which is one of numerous organizations of the Universal Accreditation Board (UAB) that governs professional PR accreditation in the U.S.

While anyone can make a mistake, and an isolated problem is one thing, the full-scale level of years upon years of PRSA’s core-integrity problems are simply inexcusable.

Turning to the culpability of (over)compensated PRSA executive staff, there are questions to be asked as well.

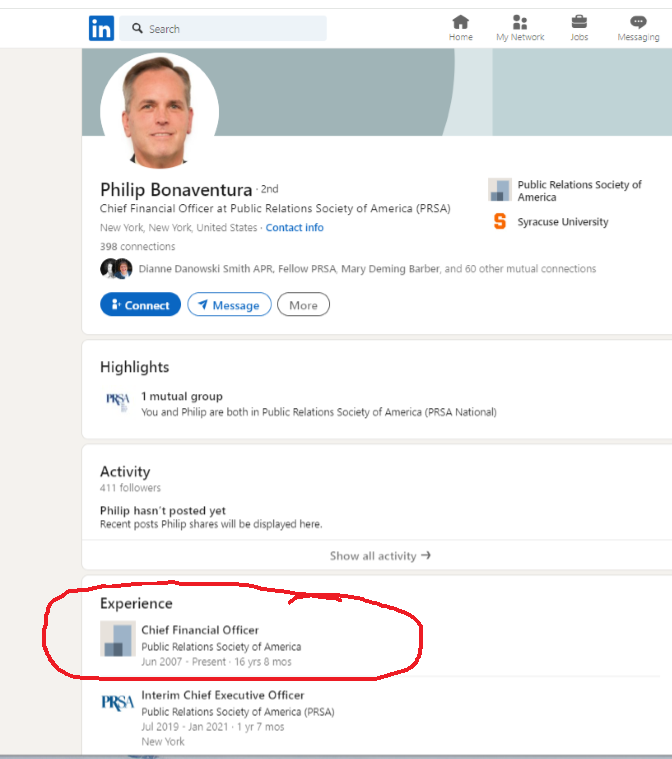

Why did PRSA CFO Phil Bonaventura – who, in fact, worked for PRSA back in 2007, according to his own LinkedIn profile documented below – direct the IRS in 2007 to send to Abreu any piece of PRSA, Inc.’s corporate tax correspondence whatsoever?

While we’re noodling on that question, the same could be asked of any number of local-level folk who also received PRSA Inc.’s IRS mailings…

There are about a dozen of these local-level PRSA chapter contacts — from such far-flung locales as Knoxville, Mechanicsburg, Wichita, Roanoke, Oklahoma City, and more — all cited by the IRS on its publicly searchable database as having received PRSA, Inc., 13-1582190 EIN 990-N postcard correspondence.

This entire situation merits a formal investigation and a call by PRSA membership to demand answers from National Board leadership, to whom the paid headquarters staff are supposed to report.

As 2024 is now upon us, I’m writing off any hope that PRSA will clean up its appalling act.

Back in 2016, little did I know that a PRSA National officer’s call for barring “I hate math!” would ultimately lead to the derailing of PRSA’s core ethics and even its legal compliance, in a twisted cultural and operational modus operandi of “I hate integrity!”

As years of my personal experiences and volumes upon volumes of clear documentation make abundantly clear, what has become baked into PRSA’s national-level organizational culture will stay there.

[…] Abreu has curiously ascended to the PRSA National Chairmanship, within weeks of PRSA posting $5.4 million in math errors to its balance […]

[…] by now that PRSA’s clown car continues to be driven by a national leadership who posted some $5.4 million in math errors on its balance sheet only months ago, in December […]